Critical Thinking is a popular domain and has application in how we tune ourselves to think objectively and minimise biases in decisions. In Credit Risk, it simply means a more logical way to evaluate customers, business cases and loan applications.

Unfortunately, the need to recognise cognitive biases and fallacies while taking credit decisions, is an ignored area. In fact, there is sense of disdain as we assume our past experience and excel templates to be good enough.

For us bankers, data-based arguments are the staple to justify our credit decisions. But often, even these ostensibly factual rationales may have inadvertent fallacies, leading to wrong inferences.

Sharing two formal Fallacies that may be important from Credit Risk perspective.

1. Fallacy of Composition: What is true for part is true for the whole.

There are many ways this may manifest in Banks.

Consider the argument– The parent company has done well with CAGR of 25% over last 5 years. Management has shown the capability to handle new businesses in the past. The new venture is in safe hands.

In a regular discussion or CAM (Credit Appraisal Memo), this is a seemingly good articulation to justify the new proposal at hand. However, there are a few logical gaps that need to be addressed.

First, the industry structures, supply chain linkages and demand side requirements may be entirely different for new business. Secondly, while you can draw comfort based on past performance, it is not a sufficient logical reasoning of what will happen in the future. Especially true for greenfield or new product category. Thirdly, if the parent company itself is doing well and growing fast, will the management have enough bandwidth to handle a new venture?

In short, the rationale, that it has worked in the past or for other parts and therefore, will work for everything, needs some critical evaluation. What seems great with partial data may not be true for whole.

2. Fallacy of Division: What is true for the whole is true for the part.

This is the reverse of FOC where a bird’s eye view is assumed to be a good justification for the things at hand.

Consider the argument – Auto industry has done well with 10% growth over last year. Industry reports suggest prices of commodities have been stable over last year hence we have a better sight on the projected profitability levels. The auto component manufacturer is therefore likely to do well.

There are two logical gaps in this presentation. First, what is true for an industry may be driven by specific market segments and may or may not be applicable to the case in hand. For e.g., Cars may have done well but, can we logically conclude that, say, an auto component manufacturer of plastic parts for commercial vehicles will also do well? Second, stability in the prices of say, steel, metals and other commodities may give an impression of predictability however oil prices have been volatile. We know plastics have direct link to crude.

In essence, over reliance on whole may lead to missing out the real micro risks.

Applying Critical Thinking to build Credit Risk Culture.

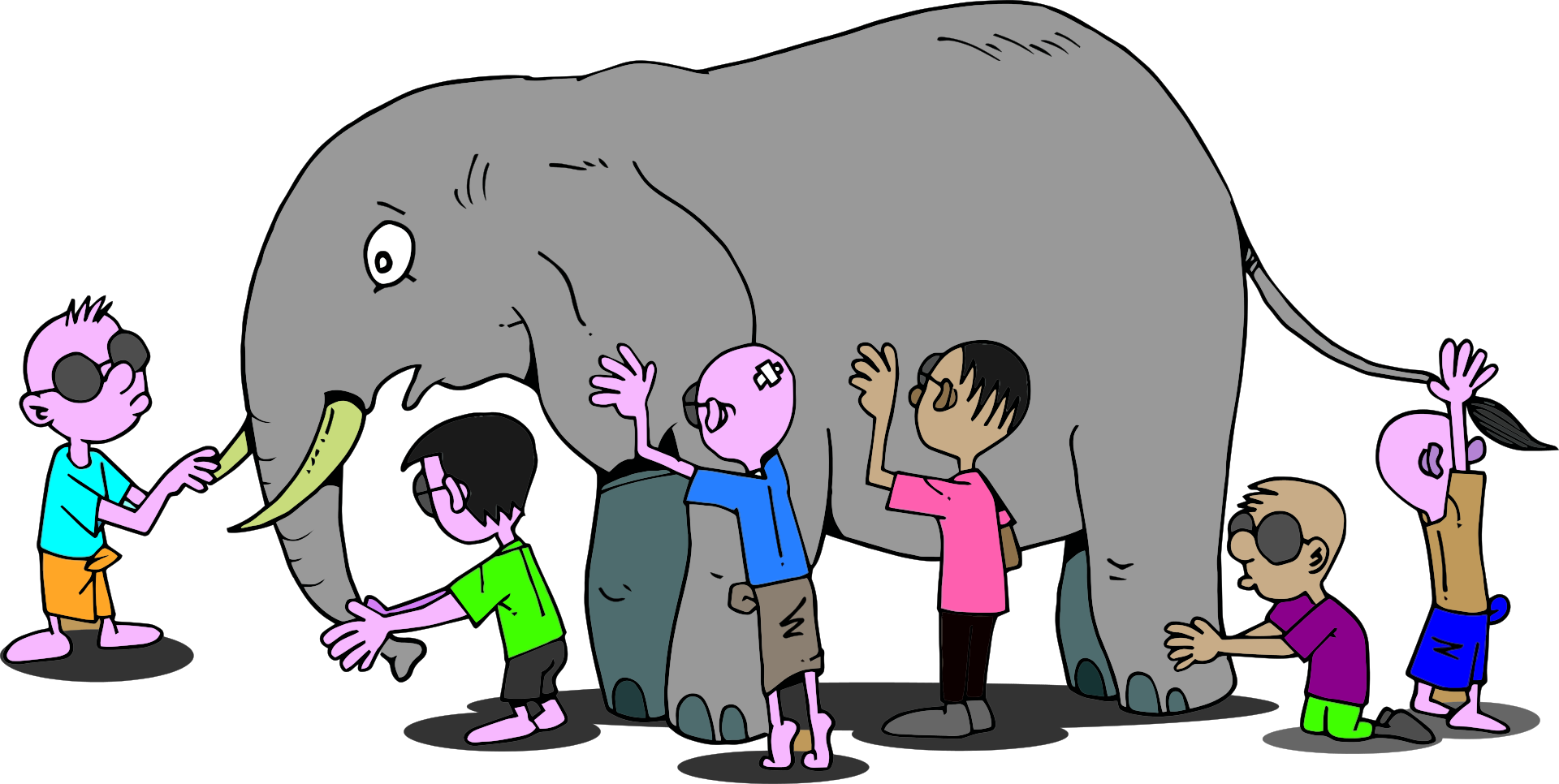

Moral of the story (including that of the picture on top), selectively placing data will lead to logical errors and incorrect conclusions. As I often reiterate in my workshops, getting enamored by bits of data leads to both wrong approvals and rejections.

Right decisioning in credit risk requires a balance between the two seemingly dichotomous aspects- First, having a wholistic view beyond selective data presentation and second, understanding the impact (materiality) of micro elements on the larger picture.

And, how do we bring this culture within teams? The first step is to sensitise the stakeholders that complete facts should prevail over our own biases, and logic takes precedence over good presentation.

Disclaimer: The opinions expressed here are those of the author and does not reflect the views of FrankBanker.com