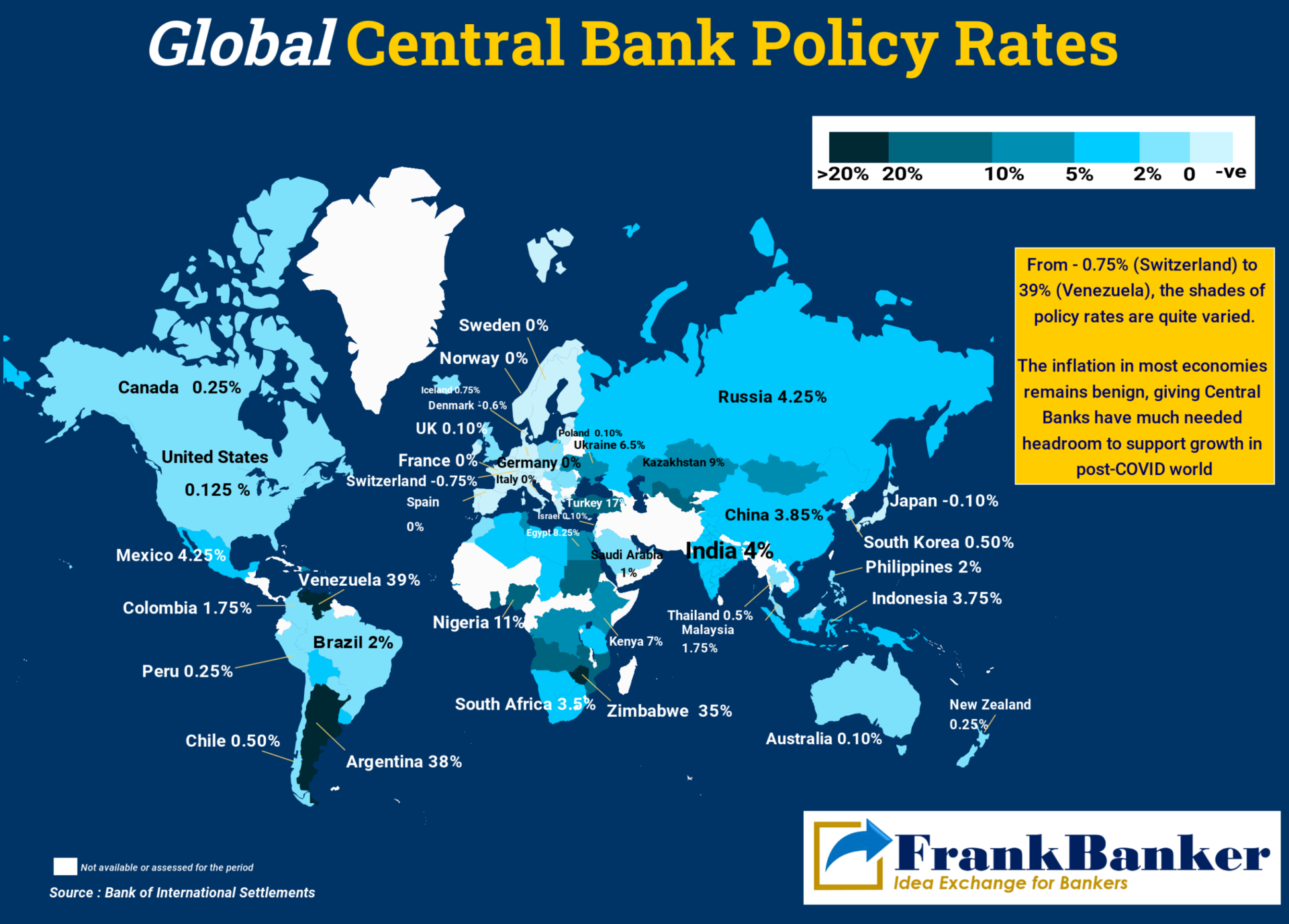

[dropcap]F[/dropcap]rom – 0.75% (Switzerland) to almost Zero in most of Europe to around 4% in India, Central Banks in most economies remain accommodative.

Although inflation remains benign in most places, some high inflation economies like Argentina (38%) and Venezuela (39%), have their plates overflowing with challenges.

While the GDP projections are encouraging, whether cheaper credit can fuel a rebound in economic activity, remains to be seen.

We at FrankBanker are hopeful!

[btn url=”https://www.frankbanker.com/wp-content/uploads/2021/03/Global-Central-Bank-Policy-Rates-1.pdf” text_color=”#000000″ bg_color=”#daa520″ icon=”” icon_position=”start” size=”14″ id=”” target=””]Download and Share[/btn]