[dropcap]O[/dropcap]ver the last few years, we have heard of Super Apps (Applications), and how they will be key and dominant players in the whole digital ecosystem. This is backed by efforts by leading players with mixed or limited success. We have known of the success of Amazon, GoJek etc. and also heard of many others who could not realise their efforts fully or effectively.

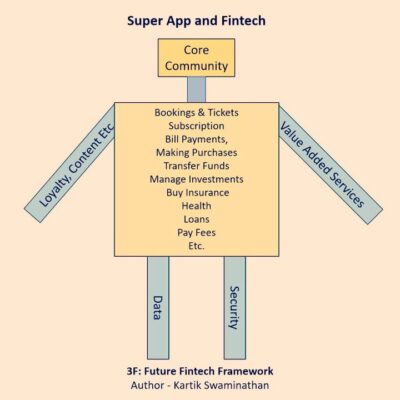

Simply put, Super Apps are Apps which aggregate and enable us to perform most of our activities digitally, like Bookings, Tickets, Subscription, Bill Payments, Making Purchases, Transfer Funds, Manage Investments, Buy Insurance, Health, Pay Fees etc. (We can keep adding many functionalities).

For an App to be a Super App, one needs a sizable community of users who frequently visit and use the app. This can then be leveraged to create an ecosystem of value-added solutions aimed at meeting various needs of your community.

This implies that players like large Retail Ecommerce Apps, Banks, Payment Companies (Like Wallets & Cards), Social Media Apps, Media Apps & OTT Apps etc are better suited to become a Super App, as they have a large community of users, who frequently visit and use the App.

There can also be Mini Super Apps, if the core propositions and wed it tightly with other complementing capabilities aimed at a community / target segment, for e.g. Stock Brokers Apps can offer a tightly curated set of solutions which will help people manage their Investments / Finances better, Similarly we can have Apps for University Ecosystem, For Resident of Housing Societies / Gated Communities.

So while Super Apps as a proposition remain relevant even today and some have demonstrated this, we cannot just create a successful Super App by just having a large community and a set of propositions (with core proposition).

So while Super Apps as a proposition remain relevant even today and some have demonstrated this, we cannot just create a successful Super App by just having a large community and a set of propositions (with core proposition).

For a Super App or Mini Super App to be really effective and successful, it also needs to create engaging user journeys which are not just Multiple Single Journeys or Simple Redirections (as is the case in many so called Super Apps), but Integrated offerings. Then we need to add layers of capabilities like effective Loyalty Programs, Content etc.

So, to do all this effectively, we will need to follow an Innovative framework called 3F: Future Fintech Framework, which allows us to Map these functionalities, add capability Layers to create an integrated offering, and then enable us to create engaging user Journeys for every use case. 3F: Future Fintech Framework enables this through Frameworks called FLARE (Fintech Logical Architecture) & FDLC (Fintech Digital Life Cycle Respectively). The best part is these frameworks are Tech, Product & Solution agnostic and can be applied to most of the App types / Functionalities as discussed above. Only external limiting part can be, availability of Partners & API’s. However, even that will be gradually addressed though another Framework proposed as part of 3F: Future Fintech Framework called FAM (Fintech API Marketplace)

So, if you are working on a Super App, Mini Super App or plan to make your existing app more appealing and engaging for your users, then 3F: Future Fintech Framework will enable you with an approach / thought process to do so.

Disclaimer: The opinions expressed here are those of the author and does not reflect the views of FrankBanker.com