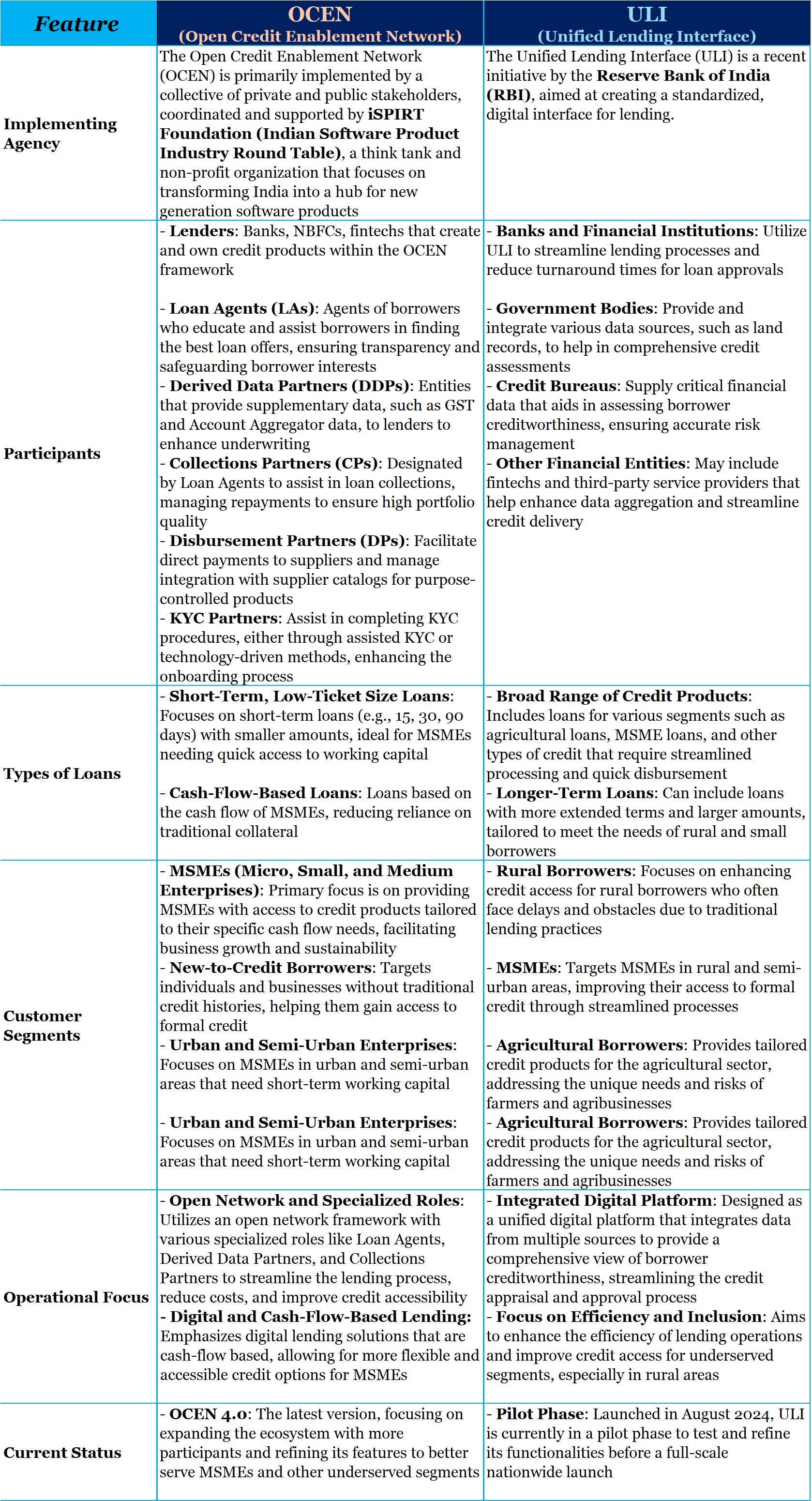

India’s journey towards financial inclusion is being revolutionized by two pivotal initiatives in its Digital Public Infrastructure (DPI): the Open Credit Enablement Network (OCEN) and the Unified Lending Interface (ULI). These platforms are designed to transform the lending landscape by making credit more accessible and streamlined for underserved segments. But how do they differ, and what unique roles do they play in enhancing India’s digital credit ecosystem?

The table below breaks down their key features and objectives

OCEN and ULI represent a dual approach to leveraging digital technology for financial empowerment in India. While each platform targets different aspects of the credit delivery process, together, they embody the future of inclusive finance. While details are still evolving, we are excited that by addressing the needs of diverse borrower segments, these initiatives are not just reshaping credit access—they are redefining what it means to participate in the digital economy.