& Ravi Kiran Gorthy

One Loan, Many Systems

Somewhere in a mid-sized lending institution right now, a credit operations officer is re-entering data that already exists in another system. The borrower’s income, employer name, and address were captured at application. They are being typed again because the Loan Origination System (LOS) and the Loan Management System (LMS) do not share the schema. This is not an edge case. It is not even a technology failure. It is exactly the way systems are designed to work.

Lending process is one continuous flow. Each loan is sourced, assessed, approved, documented, booked, serviced, monitored, and collected. For the borrower this is one loan journey. For the lender it is one application, one loan, one risk. Yet the technology that supports it is frequently broken into separate systems, separate owners, separate vendors, and separate commercial contracts.

CRM sits here. LOS sits there. Credit scoring has its own layer. LMS becomes another domain. Analytics is elsewhere. Integration then appears as a separate exercise and as a separate business model for vendors. The result is an architecture that no one would consciously design, but that everyone has inherited.

Rational Parts, Irrational Whole

It would be easy to make this sound like a story of ignorance, incompetence, or irrationality. But the interesting truth is the stakeholders each have a rationale to this, however absurd.

Vendors are being rational when they extend product lines, preserve installed positions, and monetise integration. Banks are behaving rationally when they postpone major transformation in favour of more cost-effective incremental augmentation or patches unless some new-age player shocks them with a new stack. Regulators are being rational by being technology-neutral, focusing on outcomes rather than prescribing architectures. Yet while each one works in their own rational frame, the industry architecture becomes more fragmented, more expensive, and more frictional.

This friction arises not because lending is fragmented but because technology has evolved in fragments, product suites have expanded over time, acquisitions have been absorbed imperfectly, and fads have often permeated the structure. What should have been ‘designed for integration’ is ‘designed as a silo’

The consequence is not merely systemic untidiness. It is cost, delay and duplication. And it shows up most clearly at the seams.

Untidy. Uneconomic. Unsafe

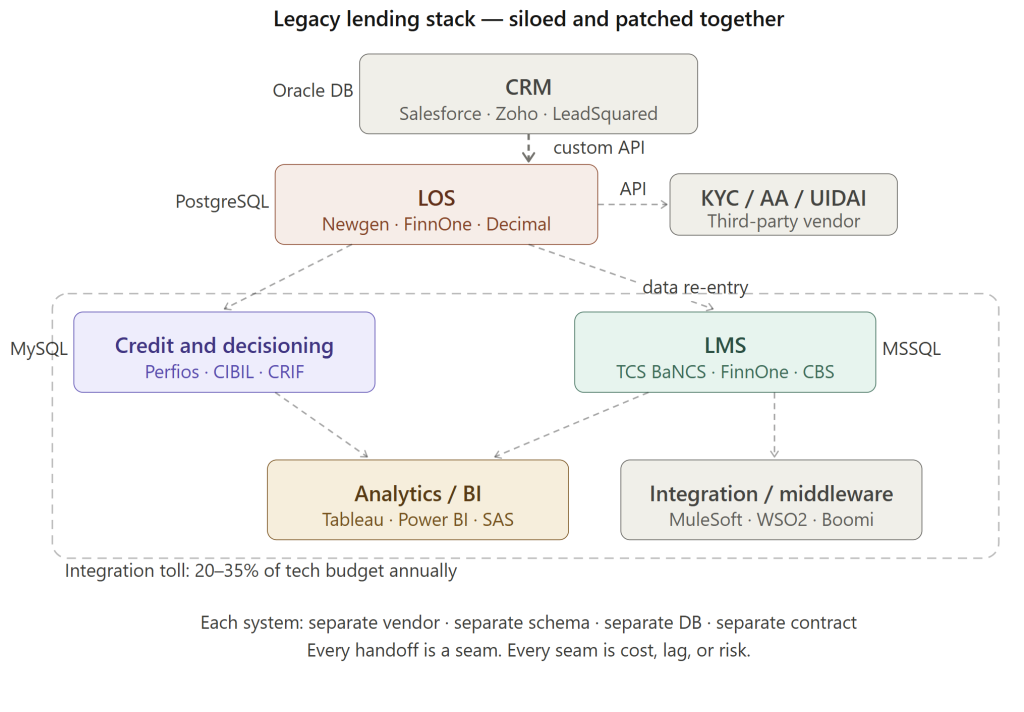

Consider the handoff between the LOS and LMS. A borrower submits income, employment, and address details at application. The LOS captures them. The loan is approved. At booking, the LMS re-captures same fields. This arises as two systems were procured at different times from different vendors and connected as an afterthought by force-fitting a customer identifier but not necessarily the data layer.

For a mid-sized lender processing 5,000 loans a month, even 15 minutes of rework amounts to 1,200 staff-hours monthly — not from inefficiency, but from architecture. That cost does not appear on any vendor’s invoice. It is absorbed quietly inside operations.

Beyond the economic costs, increased operational risk and data lag leading to monitoring gaps and reporting delays are genuine issues. Hand off from one system to another requires a documentary reference or a physical file, creating paper-based redundancy even in institutions that consider themselves fully digital.

Multiply that across origination, underwriting, servicing, and collections, each with its own data re-entry, its own format translation, its own handoff overhead, and we have a significant structural drag. The user experiences this as delay. The bank experiences it as operating cost. Although, technology providers experience it as integration scope.

The Integration Toll

Integration is the rational solution to fragmentation but suppresses a more fundamental question: should these boundaries even exist?

In mid-tier banks and NBFCs, 20 to 35% of the technology budget goes to integration maintenance, as systems are patched up, upgraded, or replaced to align with newer deployments. This is recurring liability that sits quietly inside every technology budget review, year after year.

For large banks, this is an expensive inefficiency. For smaller lenders like Cooperative Banks, small NBFCs, Credit Societies and MFIs, it is closer to a structural exclusion. While a large bank moves ahead by absorbing this ‘integration toll,’ smaller ones try to avoid it through continued physical hand-offs, maintaining data redundancy, until something breaks. Fragmentation of lending stack is not just a technology problem. It is an access problem.

In a dynamic regulatory and market environment the problem is compounded as even a recent system can turn into burdensome legacy within a few years. But legacy does not automatically mean obsolescence. The issue arises when systems are architected to trap business logic in inaccessible places, with hidden plumbing, making these systems difficult to integrate. When a monolithic point solution is sold as modular, accommodating new regulatory requirements becomes expensive.

Vendors have incentives to preserve this comfort as their large clients can afford it. This predictably creates conditions where incoherent solutions persist well beyond what the technology frontier would permit.

New Architectures — The Fad, Reality and AI

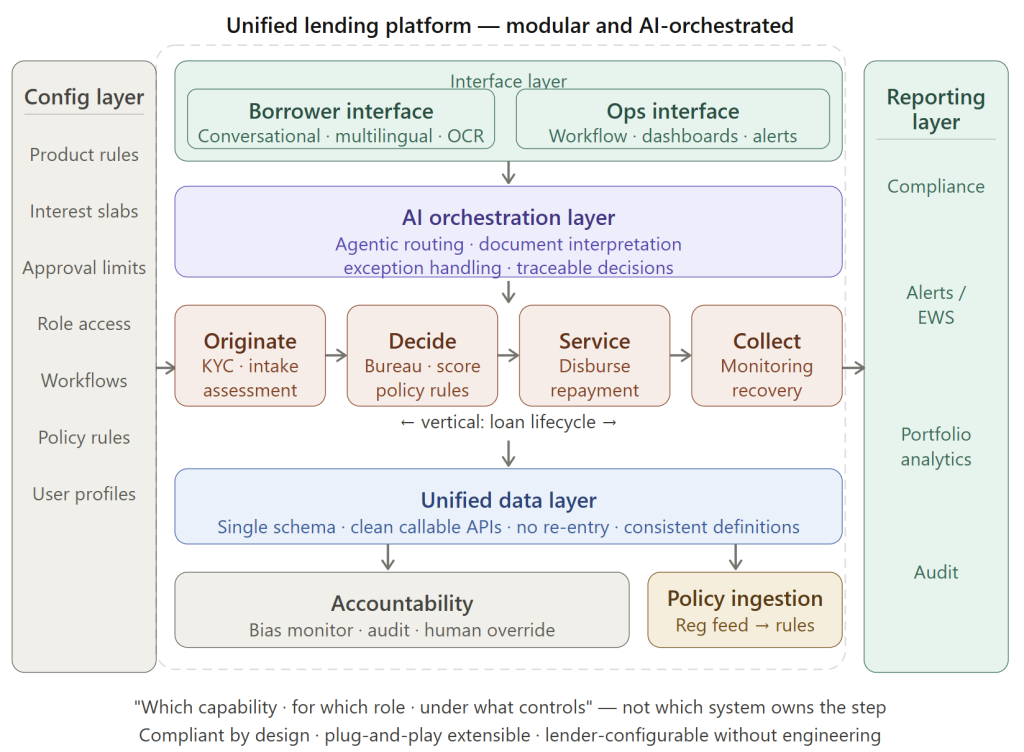

While these stack challenges are real, the technology world has not been static. API-first design, composable banking, event-driven architecture, and capability-based design represent a genuine shift from treating lending stack as a set of post facto integrated products, towards configurable capabilities that can be orchestrated.

The shift has produced its own excesses and undulations, though. Using Blockchain for credit approval system, a trusted and role-based workflow, is an overkill. Similar Composable architecture without discipline has produced setups with thousands of microservices without efficient orchestration and observability. Fad-driven modernisation does not solve the seam problem. It redistributes it.

AI has changed rules of the integration game. Agentic systems that gather data, interpret documents, route exceptions, and coordinate actions across platforms are already emerging. Unlike Robotic Process Automation (RPA) this embeds intelligence to take decisions.

The foundation of a practical AI lending system is clean data, consistent definitions, clear permissions, human guardrails, and most importantly traceable decision paths. Without that, AI does not create intelligent lending. It automates fragmentation at greater speed and with less visibility.

To our understanding, an honest architectural rethink is rather modest in approach. It asks whether the key capabilities required for the lending process — KYC, customer data, credit assessment, document verification, disbursement, repayment — can be exposed as clean, callable services with a consistent information schema. With this approach, the architecture question shifts from which system owns this step, to which capability is exposed to what role, under what controls. This grounding keeps the use case at the core while the complexity of technology, with or without AI, at the backend.

Rethink the Stack — No Longer a Stack

The key fundamental change is not in the architecture alone but in how lending software is built and operated.

- AI-assisted development is compressing build timelines and lowering the cost of generating and maintaining working code. Cloud-native, modular, API-exposed platforms can now be deployed at a fraction of earlier cost. For small lenders like Cooperatives or small NBFCs, this is the first genuinely viable path to a coherent lending stack- incrementally deployable and extendable without a six-month integration or a year-long core replacement. The impact is already trickling in. JP Morgan Chase is redeploying capital into AI-native development, with 65% of applications on the cloud and 40,000 engineers using AI coding assistants. HSBC is retiring a third of its application portfolio by 2028, calling it fundamental reengineering. In essence, the SDLC paradigm is changing.

- Focus on architecture of accountability and not just the architecture of capability. In regulated lending ‘the model decided’ cannot substitute for accountability. AI cannot be judged only by whether it works efficiently. It must be explainable, auditable, and controllable. At this stage the thinking around AI controls is evolving. Bias monitoring, decision traceability, human override mechanisms will increasingly be embedded components rather than custom enterprise builds. The systems need to be compliant by design.

- The interface layer is changing just as fundamentally, moving from form-based systems to conversational agents, with multilingual speech and text capabilities and high accuracy OCR.

- And ultimately, building unified solutions with high configurability to accommodate lender specific requirements, with role-based access controls, embedded compliance and plug and play ease, with no seams to stitch.

These collectively imply leaner, cohesive, and controllable platforms with AI-powered backend orchestration. Each meaningful work is below the demo layer, in data foundations and platform architecture.

The future of lending technology will not belong to those with the newest apps or the loudest AI claims. It will belong to those who understand that the stack was never the point. The lending process was.

References

- Boston Consulting Group. Tech in Banking 2025: Transformation Starts with Smarter Tech Investment. 6 May 2025.

- BIAN. Semantic API Practitioner Guide V8.1. December 2024.

- McKinsey & Company. Rethinking enterprise architecture for the agentic era. March 2026.

- Office of the Comptroller of the Currency. Model Risk Management, Comptroller’s Handbook; see also OCC Bulletin 2025-26. September 2025.

- Consumer Financial Protection Bureau. CFPB Issues Guidance on Credit Denials by Lenders Using Artificial Intelligence. 19 September 2023.

- Deloitte. 2026 Banking and Capital Markets Outlook. 30 October 2025.

- Deloitte. Modernizing Legacy Systems in Banking. Accessed March 2026.

- Deloitte. AI and bank software development. 24 April 2025.

- Google Cloud / DORA. Accelerate State of DevOps Report 2024.

- JPMorgan Chase. Full Investor Day 2025 Presentation. 19 May 2025.

- HSBC. Annual Report and Accounts 2025 / Q4 2025 Earnings Call. 25 February 2026.

Disclaimer: The opinions expressed here are those of the author and do not reflect the views of FrankBanker.com