Get Rich Quick?

There are two widely discussed trends circulating nowadays —first, the slowing Bank Deposit mobilisation by banks; second, the increasing retail participation in equity markets. Put together, analysts suggest a causal relationship between the two. To further corroborate this, some point to the rising Futures and Options (F&O) volumes, indicating a speculative, “get-rich-quick” mentality that may harm the economy.

While there is some merit in linking the higher risk appetite of a young population to the potential decline in CASA and Term Deposits, this argument often misses a crucial point: investors, big or small, seek value—a balanced mix of risk and reward. It’s reasonable to be concerned that investors should understand the risks involved, but positioning bank deposits as the holy grail of investments is, at best, misguided and, at worst, deliberately misleading.

The underlying question is – Are bank deposits designed to provide value to the depositor?

Cover Charges always greater than Winnings?

Fixed or Term Deposits (FDs) target the risk-averse ‘depositors’ with the proposition of safe returns with premium for capital protection. However, the problem lies in the inherent skew bank deposits have towards this ‘premium for safety’ instead of trying to achieve an optimal balance between risk and reward.

Consider an FD offering 6% nominal interest in an environment where inflation is 5%. Using the Fisher equation, the real return is:

It seems obvious that for capital to be protected-or, more optimistically, growing- FD rates should be higher than inflation. The reality, however, is far less consistent.

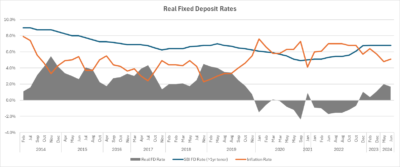

The below graph shows how real rates have moved over the last decade. There have been many instances where FDs barely outperform cash in a locker. This trend of negative or low returns is common in many countries, particularly during high-inflation periods. Paradoxically, while lending rates rise swiftly in response to policy rate changes triggered by inflation, FD rates rise rather slowly.

There are additional considerations. Headline inflation, like other macro indicators, is a directional aggregate with pre-defined weights of selected items in a basket. So, in recent times while items like housing rentals, cost of education and health have risen significantly, the moderate level of inflation may not always capture the real erosion of purchasing power. Ideally, FD rates should buffer for this inadequacy- but they often do not.

Apart from the time-value and inflation issue, FDs have other costs and constraints that ultimately reduce returns.

Rigged Roulette wheel?

Beyond the policy rates there are other behind-the-scenes factors that may be impacting FD rates. First, there are operational costs for banks—both in the origination and maintenance of deposits. Next, FDs are secured to by Deposit Insurance (DICGC in India secures deposits upto ₹5 Lakhs) and banks pay premium for this coverage. Thirdly, the bank level riskiness needs to be factored, determined by the financial standing, revenue diversification and scale of business. Lastly, there is a cost of regulatory liquidity measures like SLR and CRR.

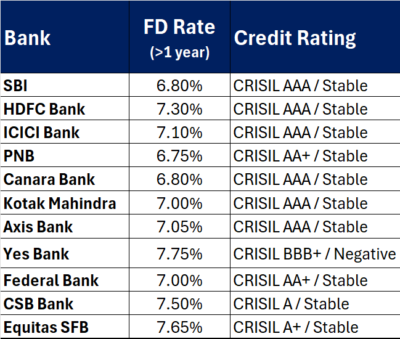

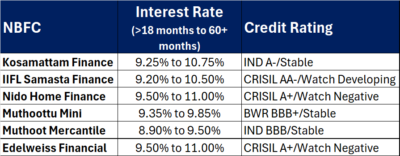

However, if you look at the FD rates across banks, they seem to be within 50-100 basis points (bps) range, indicating a low correlation with either the costs or riskiness. In contrast NBFC Non-Convertible Debentures (NCDs) or other debt instruments seem better priced for risk and aligned to market demand and supply. The comparative here is not about whether banks are safer than NBFCs- but about the relatively transparency in the process.

If all that a bank needs is to adjust 50 BPS, regardless of its risk profile or costs, it raises doubts about whether FDs rates even consider maximising value for the depositor. This anomaly from normal market behaviour can occur only if the deposit rates are systemically underpriced to the benefit of banks, rendering individual bank costs, risks and competitive pressures largely irrelevant.

Add to this pre-closure charges on FDs or, more recently, RBI’s draft proposals on higher run-off factor for digital deposits, which ultimately penalise depositors for seeking liquidity.

In short, bank deposits seem to be a structural intervention for controlling money flows, skewed more towards protecting a Bank’s Asset-Liability Management (ALM). Depositor safety looks like a side-benefit. Both CASA or Term Deposits operate within an artificial terrarium that shows a green and safe ‘investment’ ecosystem to the depositors. The real world of investment, with true risk-reward determination, operates outside its glass walls.

It’s easy to infer then, that bank deposits are not an investment product by design, and it is unfair to compare them to equity. The profile of ‘depositor’ looking for safety is not the same as that of ‘investor’ seeking growth and returns.

As more depositors wear an investor hat and see through these inefficiencies, FDs lose their appeal compared to other asset classes. Historically, Gold has always been an option and more recently, Equity investments, which do carry their own risks and moods. However, with only 6% of India’s population participating in equity markets, compared to 55% in USA and 10% in China, any growth here is a systemic positive, unlocking more efficient funding avenues for businesses, like what the recent SME IPO frenzy indicates.

Deposits are safe. But only so.

The current economic structures are designed with regulators at the center of action. Lessons of history prove that a laissez faire approach to capitalistic ideals ultimately leads to chaos where only the fittest survive and ulterior motives create havoc. Money matters are complex, and it is difficult for everyone to understand the game. So, need for a system that protects the vulnerable is a fair intention.

All said, bank deposits remain relatively safer option for a large section of uninformed investors due to this regulatory safety net, however, the question to ask is – is this a system that optimises risk-reward or has turned into a game rigged in favour of banks, completely ignoring the value proposition for depositors?

It would appear that Banks rely on inertia, gullibility or lack of awareness of the depositor, while leaning on the regulatory shoulders to sustain their liabilities book. There seems to be little incentive or competitive pressure to offer increased value or to innovate.

The paradigm needs a shift to ensure some innovation and at the very least some semblance of fair play. Needless to say, regulator is the dealer here.