Big Strategic Question: “What is the best business model for SME Finance?”

Small Simple Answer : “There isn’t one.”

In case you have been convinced otherwise, the experience shows that any templated approach, in the garb of ‘it having worked earlier’, will likely lead to loan portfolio casualty. There are two macro factors that may be our directional pointers before we navigate the deep waters of SME Lending.

Firstly, SME is not a homogenous segment and has large variance in size and scale. Definition of ‘What is a SME’ varies widely across the world. Hence straight jackets wont fit.

Secondly, the legal, regulatory and supply chain ecosystem in which the SME/MSMEs operate are significantly different, not only amongst countries but also within each. These ecosystem constraints define ‘how’ and ‘what’ of SME lending.

While both issues are interlinked, we try to evaluate these separately for better strategic clarity. But the caveat remains- there is no universal, straight, simple or exotic strategy that can be applied to SME lending. It requires deeper thought.

1. SME is not a homogenous segment

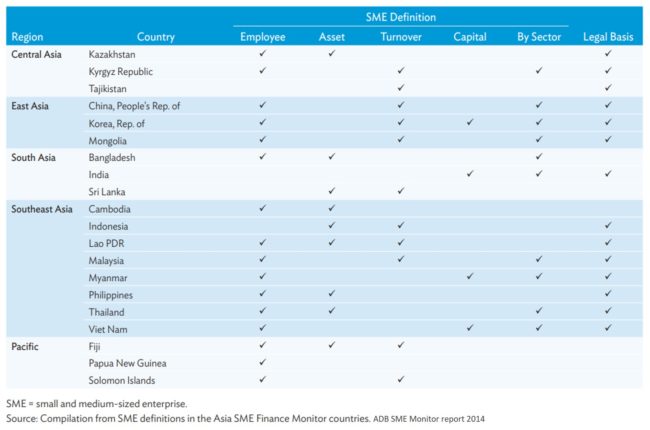

‘What is an SME?’ has no all-encompassing answer. What is Small for one is possibly Medium (or Micro) for another. Below chart indicates how the classification varies within Asia Pacific, with different countries applying different criteria.

‘Number of employees’ is another common measure but the yardsticks are of varying length. In Europe, the cut-off is 250 employees with a turnover criterion of €50 Mn, while in US it is 500 employees. For some sectors in China the employee strength for an SME is 1000 employees while in Thailand it is 200 employees. India on the other hand is augmenting its decades old ‘Investment in Fixed Assets’ based definition to Turnover-based cut off. Amongst high income Asian countries, in Japan the upper limit for SME is $2.9 Mn Assets while in neighbouring South Korea it is $6.9 Mn. In contrast, in Indonesia, it is $0.9 Mn.

While it is a moot point whether such asset, turnover or investment-based benchmarks help in a clean and clinical identification, there is one broad agreement amongst policy makers – SMEs are ‘non-corporates’. This, of course, is as ambiguous as any definition can get.

Beyond the difference on account of size of economy, the policy definitions are primarily designed to identify most vulnerable sections. For lenders, these classifications may not be practical. Most banks, therefore, calibrate these with their own cut offs. For example, in two large private sector banks where I have worked, one used the ‘Networth’ of the entity as the criteria while the other used ‘Turnover’ based cut offs. These are not necessarily aligned to the regulatory definitions but based on expert view (read ‘gut feel’) for easy borrower identification at the time of loan origination.

This heterogeneity in ‘What is a SME’ is not limited to regulatory definitions. Even within a country, SMEs have significant variance in the products and service they deal in. This ranges from high value-add manufacturing clusters to low margin wholesale commodity trading businesses to neighbourhood grocery stores. The operating cycles, capital requirements, market support and risks of each vary significantly.

Add to this the cultural aspects of how the borrowers see the loan– a desperate measure (loan is bad) , an obligation (a fair commercial transaction to be paid off) or a subsidy. Then there is demographic dynamics at play- gender, community, education etc.

In short, nuances for each sub-market may vary substantially and hence assuming one standard evaluation or distribution model for SME finance will be erroneous. The many examples of multi-national banks faltering with aggressive SME lending in newer markets, stand witness to it. The multi-tiering of lenders (Banks, NBFI, Micro Finance etc) is another reflection of this complexity.

Viewing the SME market as conglomeration of multiple business cohorts or clusters is a more scientific and practical first step to building a robust SME strategy. (For more research minded, some of the reports at the end can help understand various definitions of SME.)

2. Ecosystem challenges- Legal and taxation

If you skim the development agencies’ and academic literature, some common themes on challenges faced by SME borrowers, emerge

a. Access, adequacy, and cost of growth capital

b. Access to professional document and accounting expertise

c. Availability of adequate collateral security

d. Delayed realisation of debtors due to negotiation asymmetry while dealing with a large corporate buyer.

This is considered to be especially true in developing markets and in some way, albeit indirectly, implicates the lenders for restricting growth of ‘gullible’ and ‘naïve’ SMEs. However, looking deeper would clearly indicate this to be an over generalisation.

While the smaller size, equity and low negotiating power are key vulnerabilities of SMEs, the real constraining factor is the legal and tax compliance ecosystem.

In many countries, either the taxation is very high (typically 30% or higher) and hence the temptation for a low margin small business to avoid tax or the tax compliance machinery is lax or corrupt. In either case much of the sales is off book, making it difficult for the lenders to ascertain financial performance of the SMEs.

Further, if the legal framework, especially recovery laws and enforcement, is weak, the lenders are compelled to adopt conservative lending policies like high promoter contribution, collaterals, and interest rates.

Similarly, a weak Contract enforcement framework makes SME suppliers vulnerable to arm-twisting (margin reduction) or delayed payments (cash flow constraints) from their large corporate buyers.

In essence, lending challenges (and opportunities) in a market cannot be simplistically linked to SME’s ability to provide documents or security or lenders’ conservatism. The legal and taxation ecosystem is the key determinant of transparency and awareness with which both can operate.

A surrogate indicator of the strength of legal framework is the way Supply Chain Finance products perform in a market. SCF primarily entails uncollateralised, transaction level financing of SMEs based on their supplies to the corporate. If the market power of the Corporate (and therefore ability to leverage the legal loopholes) is highly asymmetric, these products cannot find traction. Such markets will then move to high collateralised lending based on averaging based methods (year-end financials) instead of cash-flow based funding.

Understanding of this ecosystem therefore drives the width and depth of the lending products that a Bank will have in a market.

Any lender/advisor building a SME strategy should consider the above macro and ecosystem variables before moving on to product and risk policy design. It takes deep dive and effort. Any navigational shortcut is likely path to turbulence.

“The pessimist complains about the wind; the optimist expects it to change; the realist adjusts the sails.” – William Arthur Ward

Reference/Further reading

https://www.adb.org/sites/default/files/evaluation-document/346336/files/eap-sme.pdf

https://www.oecd.org/cfe/smes/adb-oecd-study-enhancing-financial-accessibility-smes.pdf

https://www.imf.org/-/media/Files/Publications/WP/2020/English/wpiea2020055-print-pdf.ashx

http://documents1.worldbank.org/curated/en/809191507620842321/pdf/Addressing-the-SME-finance-problem.pdf

https://www.adb.org/sites/default/files/publication/214476/adbi-smes-developing-asia.pdf

https://msme.gov.in/know-about-msme

https://msme.gov.in/sites/default/files/RBI-NOTIFICATION.pdf

https://taxfoundation.org/publications/corporate-tax-rates-around-the-world/#Changes